How Mobile Banking Is Changing the Way People Save and Spend in Kenya

Read Time:3 Minute, 27 Second

Mobile banking has transformed Kenya’s financial landscape, reshaping how people save, spend, and access money. Over the past two decades, the country has become a global reference point for mobile money services, led by the success of M-Pesa and a rapidly advancing digital ecosystem.

This mobile banking revolution in Kenya has made financial tools more accessible, affordable, and secure, particularly for those previously excluded from the formal banking system.

Accessibility and Financial Inclusion

One of the most important ways mobile banking has changed saving and spending in Kenya is by expanding access to financial services. Traditional banks once remained out of reach for many citizens, especially in rural areas, due to high costs, long distances, and documentation requirements.

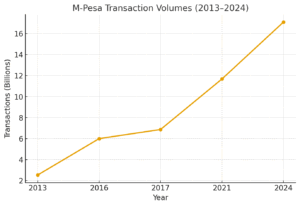

The launch of M-Pesa in 2007 changed this model, enabling users to deposit, withdraw, transfer, and save using basic mobile phones without needing a traditional bank account.

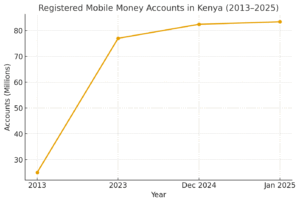

By 2023, Kenya recorded about 77.3 million registered mobile money accounts, far exceeding its population of 51.5 million. This shows widespread adoption and, in many cases, multiple accounts per individual.

According to the 2021 FinAccess Household Survey, formal financial account ownership in Kenya rose to 84% in 2021, up from 83% in 2019. Today, more than 80% of Kenyan adults rely on mobile money services for payments and savings.

Changing Saving Habits

Mobile banking has reshaped savings behavior by introducing digital tools that support small but consistent contributions. Services such as M-Shwari, integrated with M-Pesa, allow users to save from as little as one shilling while earning interest of up to 6.3% annually.

Other platforms, including the KCB Mobile App, offer goal-setting features, automated savings, and real-time tracking to encourage disciplined saving.

These services have enabled small-scale traders, farmers, and salaried workers to build financial cushions. Research shows that M-Pesa users are more resilient to income shocks, as digital savings and transfers help households maintain consumption during crises.

Apps like Chumz, licensed by the Capital Markets Authority, further support structured savings through user-friendly mobile platforms. The shift away from informal methods such as cash storage at home has improved financial security and reduced risks of loss.

New Spending Patterns

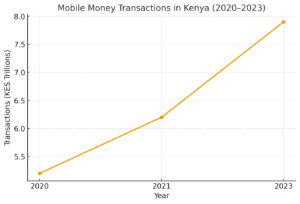

Mobile banking has also changed how people in Kenya spend. Mobile money transactions in Kenya reached KES 6.2 trillion in 2021. From utility bills to school fees, payments are increasingly made through mobile platforms, eliminating the need for cash handling.

Banks and fintechs have also developed applications to make spending more transparent.

For instance, the KCB Mobile App includes spending visualizations, while Equity Bank’s One Equity Till Number allows merchants to accept payments from multiple channels without extra charges. These innovations have simplified everyday transactions for both businesses and consumers.

In 2022, mobile banking was the preferred digital service among bank customers in Kenya, accounting for nearly 70% of all digital interactions. The convenience and speed of transactions continue to make mobile banking the dominant choice over alternatives such as internet banking.

Economic and Social Outcomes

The adoption of mobile banking has contributed to measurable economic gains. A 2016 study found that M-Pesa lifted 194,000 households, or 2% of the national total, out of poverty between 2008 and 2016 by improving consumption.

Women in particular have gained financial independence through mobile services, using them to save, invest, and run businesses.

Mobile money’s contribution to the economy is substantial, accounting for about 56.8% of Kenya’s GDP in 2021. Yet challenges remain, including high loan fees, such as M-Shwari’s 7.5% charge for 30-day loans, and cybersecurity risks from fraud and scams.

The Road Ahead

The future of mobile banking in Kenya is expected to expand further as regulators and banks explore innovations such as a Central Bank Digital Currency (CBDC). Investments in IT infrastructure are rising, with many banks dedicating larger shares of operating expenditure to digital platforms.

Jefferson Wachira is a writer at Africa Digest News, specializing in banking and finance trends, and their impact on African economies.

Happy

0 %

Sad

0 %

Excited

0 %

Sleepy

0 %

Angry

0 %

Surprise

0 %

Average Rating